Implementing Alternating Least Squares (ALS) from Scratch in Python

A deep dive into building ALS for recommendation systems in Python. Includes the full derivation, a vectorized implementation, and an analysis of its real-world performance limits.

Alternating Least Squares (ALS) is a cornerstone of classic recommendation systems. But how well does a pure implementation actually perform on a real-world dataset like MovieLens? I built it from scratch in Python to find out. In this lab, we’ll derive the math, build an efficient vectorized implementation, and discover a surprising truth: without specific modifications, it can fail to beat even simple baselines. Here’s the full story.

The Matrix Factorization Problem

In recommendation systems, we typically have:

- A set of users

- A set of items

- A sparse matrix of known ratings or interactions

Let’s call this sparse matrix where represents user ‘s interaction with item . Most entries in are missing.

The basic ALS formulation is particularly useful in implicit feedback settings, where zeros are assumed to be meaningful rather than missing data. This approach is commonly used in implicit recommendation systems, such as collaborative filtering for user interactions (e.g., clicks, purchases, or views).

However, in explicit feedback settings (e.g., movie ratings), missing values should be properly handled to avoid bias in factorization.

The goal of matrix factorization is to approximate as the product of two lower-dimensional matrices:

Where:

Each row of represents a user’s latent preference vector, which encodes how much they tend to interact with certain hidden factors. Likewise, each row of represents an item’s latent feature vector, which captures how strongly an item aligns with those same factors. These vectors are learned such that their interactions best approximate the observed data in , revealing patterns in user behavior and item similarities.

Solving a Non-Convex Optimization Problem

To reiterate, we aim to approximate using two lower-rank matrices, capturing the latent structure in the data:

This is a non-convex optimization problem because both and are unknown and multiply each other. Simultaneously optimizing both matrices would require solving a problem with multiple local minima, making direct gradient-based optimization difficult.

Why ALS Works

Instead of solving for both and at once, Alternating Least Squares (ALS) breaks the problem into two convex subproblems:

- Fix and solve for

- Fix and solve for

Since each of these steps is a standard least squares problem, they have a closed-form solution that can be computed efficiently.

Setting Up Our Example

Let’s create a small example with synthetic data to demonstrate ALS.

import numpy as np

np.set_printoptions(precision=3)

np.random.seed(42)users = 50

items = 30

features = 10The following matrix represents our sparse user-item interaction matrix. For simplicity, we’re using binary values (0 or 1) to indicate whether a user interacted with an item:

R = np.random.choice([0, 1], size= [users,items], p=[.9, .1])

Rarray([[0, 1, 0, ..., 0, 0, 0],

[0, 0, 0, ..., 0, 0, 0],

[0, 0, 0, ..., 0, 0, 0],

...,

[0, 0, 0, ..., 0, 0, 0],

[1, 0, 0, ..., 0, 0, 0],

[0, 0, 0, ..., 0, 0, 0]], shape=(50, 30))Here we initialize our user and item latent factor matrices with random values from a normal distribution. In a real application, we might use different initialization strategies:

U = np.random.normal(0,1, [users, features])

V = np.random.normal(0,1, [items, features])Understanding the ALS Updates

Matrix factorization assumes we approximate using two lower-rank matrices and :

To find optimal values for these matrices, ALS alternates between solving for with fixed and vice versa. This alternating approach makes each sub-problem convex, guaranteeing a unique global minimum at each step.

Let’s illustrate this clearly by deriving the update rule explicitly for one row of :

-

For each row :

This corresponds to solving the least squares problem1:

Expanding the squared term gives:

Since we fixed , this function is convex in , and the minimum is found by setting the derivative to zero:

Simplifying, we have:

Recognizing the matrix forms:

we obtain the closed-form solution:

-

For each row :

Which leads to the least squares update:

Now, instead of iterating over rows, these updates can be vectorized for efficiency and conciseness:

-

Solving for in matrix form:

-

Solving for in matrix form:

Solving the Least Squares System with numpy.linalg.solve

The least squares updates derived above involve computing matrix inverses. However, explicitly computing the inverse (or pseudoinverse) can be numerically unstable. Instead, we solve the linear system directly using numpy.linalg.solve, which finds the solution ( X ) to the equation:

where and (for solving ), or and (for solving ).

Thus, the least squares updates can be computed efficiently and with better numerical stability as:

We will use this formulation in the ALS implementation below.

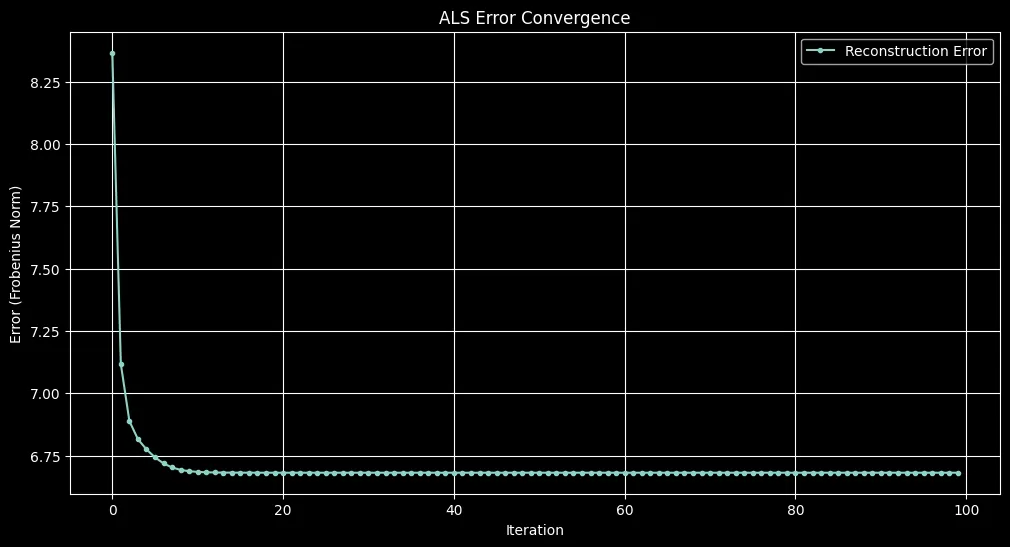

# Compute initial reconstruction error

prev_score = np.linalg.norm(U @ V.T - R)

# Store errors for visualization

errors = [prev_score]

# ALS Iterations

num_iterations = 100

for iteration in range(num_iterations):

# Without vectorization (per-row computation)

# for i in range(U.shape[0]):

# U[i] = np.linalg.pinv(V.T @ V) @ V.T @ R[i]

# Equivalent vectorized forms for solving U:

# U = (np.linalg.pinv(V.T @ V) @ V.T @ R.T).T

# U = R @ V @ np.linalg.pinv(V.T @ V)

U = np.linalg.solve(V.T @ V, V.T @ R.T).T # numerically stable solution

# Without vectorization (per-row computation)

# for i in range(V.shape[0]):

# V[i] = np.linalg.pinv(U.T @ U) @ U.T @ R[:, i]

# Equivalent vectorized forms for solving V:

# V = (np.linalg.pinv(U.T @ U) @ U.T @ R).T

# V = R.T @ U @ np.linalg.pinv(U.T @ U)

V = np.linalg.solve(U.T @ U, U.T @ R).T # numerically stable solution

# Compute and store error after each iteration

errors.append(np.linalg.norm(U @ V.T - R))

# Compute final reconstruction error

final_score = errors[-1]

print(f"Initial error: {errors[0]:.4f}")

print(f"Error after 1 iteration: {errors[1]:.4f}")

print(f"Final error after {num_iterations} iterations: {final_score:.4f}")

Initial error: 120.4196

Error after 1 iteration: 8.3655

Final error after 100 iterations: 6.6819import matplotlib.pyplot as plt

plt.style.use('dark_background')

plt.figure(figsize=(12, 6))

plt.plot(errors[1:], marker="o", linestyle="-", markersize=3, label="Reconstruction Error") # Exclude the first error value to better visualize the convergence process without the initial large drop.

plt.xlabel("Iteration")

plt.ylabel("Error (Frobenius Norm)")

plt.title("ALS Error Convergence")

plt.legend()

plt.grid()

plt.show()

Regularized ALS

In practice, it’s common to add regularization terms to ALS to prevent overfitting and improve numerical stability. Regularized ALS optimizes the following loss function:

This leads to the regularized update equations:

Regularization is especially valuable when working with sparse datasets, as it helps avoid singular matrix issues during matrix inversion steps.

Weighted ALS (WALS)

Weighted ALS generalizes ALS by assigning different importance (weights) to observed ratings. This method is particularly beneficial in explicit feedback scenarios, such as rating systems (e.g., movie ratings), where some items or users have significantly more interactions than others. By applying weights, WALS compensates for this imbalance, boosting underrepresented items and improving recommendation fairness.

WALS optimizes the following loss function:

Here, each rating’s squared error is scaled individually by a weight (w_{mn}).

Choosing the weights

Inspired by this resource2, we propose a practical method for computing these weights, accounting for item popularity:

- Each weight (w_{mn}) is computed as a baseline plus a scaling factor dependent on how frequently the item (n) has been reviewed:

- is a baseline weight, ensuring every interaction has a minimal influence.

- is the number of non-zero ratings for item (n), representing the item’s popularity.

Two common choices for the scaling function (f(c_n)) are:

-

Linear (explicit) scaling, suitable for explicit feedback datasets (such as movie ratings):

Here, more popular items (higher (c_n)) receive lower additional weight, balancing their influence.

-

Exponential (implicit) scaling, suitable for implicit feedback scenarios (such as clicks or views):

This sharply decreases the influence of very popular items, controlled by the exponent (e).

Weighted ALS Update Step

When performing updates in WALS, the weight vector for each user or item is transformed into a diagonal matrix by multiplying with the identity matrix:

-

For user factors (U_m):

-

For item factors (V_n):

In these equations, and explicitly create diagonal matrices from weight vectors (w_m) and (w_n), respectively, ensuring that each interaction is weighted correctly and independently.

A complete, efficient implementation of Weighted ALS using these updates will be provided in the full code example at the end of this blog post.

Alternatives and Extra Resources

While ALS and its weighted variant are effective, other optimization methods like Stochastic Gradient Descent (SGD) are frequently employed:

- Stochastic Gradient Descent (SGD) updates parameters iteratively, adjusting each user-item interaction individually. This characteristic makes SGD well-suited for online recommendation systems, though typically slower for large batch-processed datasets.

Notable resources and advanced readings include:

- “Fast Matrix Factorization for Online Recommendation with Implicit Feedback”3, presenting efficient algorithms specifically tailored for implicit-feedback online scenarios.

These alternatives and resources are valuable considerations when adapting matrix factorization methods to diverse real-world scenarios.

Conclusion

Alternating Least Squares is a powerful technique for matrix factorization in recommendation systems. The algorithm’s key advantage is that it handles the non-convex optimization problem by alternating between convex subproblems, each of which has a closed-form solution.

While more advanced techniques like neural collaborative filtering have emerged in recent years, ALS remains relevant for its simplicity, interpretability, and effectiveness, especially for large-scale recommendation tasks.

Full Python implementations

import numpy as np

# ---------- weighting utils ----------

def linear_weight_fn(c_n, w0: float = 0.1, wk: float = 1.0):

"""Per-item popularity weights; smaller extra weight for very popular items."""

return w0 + wk / (c_n + 1e-8)

def make_mask(R: np.ndarray, zero_means_missing: bool = True) -> np.ndarray:

"""

Build observation mask M.

- If zero_means_missing: treat 0 as missing (implicit/binary clicks).

- Else: any entry counts as observed (or non-NaN for float matrices).

"""

if zero_means_missing:

return (R > 0).astype(float)

return (~np.isnan(R)).astype(float) if np.issubdtype(R.dtype, np.floating) else np.ones_like(R, dtype=float)

def item_weights_from_mask(M: np.ndarray, weight_fn=linear_weight_fn) -> np.ndarray:

"""Compute per-item weights from popularity (column sums of M)."""

c_n = M.sum(axis=0) # popularity per item

return weight_fn(c_n) # shape: (items,)

# ---------- metrics ----------

def observed_rmse(R_true: np.ndarray, R_pred: np.ndarray, M: np.ndarray) -> float:

num = ((R_true - R_pred)**2 * M).sum()

den = M.sum()

return np.sqrt(num / max(den, 1))

def weighted_rmse(R_true: np.ndarray, R_pred: np.ndarray, w_item: np.ndarray, M: np.ndarray) -> float:

W = M * w_item # broadcasts over columns

num = ((R_true - R_pred)**2 * W).sum()

den = W.sum()

return np.sqrt(num / max(den, 1))

import numpy as np

def als_with_regularization(

R: np.ndarray,

rank: int = 10,

iters: int = 100,

reg: float = 0.1,

*,

zero_means_missing: bool = True,

seed: int | None = 42,

dtype=np.float32,

):

"""

Unweighted ALS. Zeros are treated as real observations inside the update;

M is returned so you can ignore zeros as 'missing' in metrics.

Returns: U, V, w_item (all ones), M

"""

rng = np.random.default_rng(seed) if seed is not None else np.random.default_rng()

users, items = R.shape

I = np.eye(rank, dtype=dtype)

U = rng.normal(0, 1, (users, rank)).astype(dtype)

V = rng.normal(0, 1, (items, rank)).astype(dtype)

Rt = R.astype(dtype)

for _ in range(iters):

Gv = V.T @ V + reg * I

U = (np.linalg.solve(Gv, V.T @ Rt.T).T).astype(dtype)

Gu = U.T @ U + reg * I

V = (np.linalg.solve(Gu, U.T @ Rt).T).astype(dtype)

M = make_mask(R, zero_means_missing=zero_means_missing)

w_item = np.ones(items, dtype=float)

return U, V, w_item, M

# ----- demo -----

users, items, rank = 50, 30, 10

R = np.random.default_rng(42).choice([0, 1], size=(users, items), p=[0.9, 0.1])

U, V, w_item, M = als_with_regularization(R, rank=rank, iters=100, reg=0.1, seed=42, zero_means_missing=True)

R_hat = U @ V.T

print(f"Observed RMSE (mask only): {observed_rmse(R, R_hat, M):.4f}")

print(f"Weighted RMSE (matches training): {weighted_rmse(R, R_hat, w_item, M):.4f}")

print(f"Full Frobenius Norm (incl. missing zeros): {np.linalg.norm(R - R_hat):.4f}")

Observed RMSE (mask only): 0.4026

Weighted RMSE (matches training): 0.4026

Full Frobenius Norm (incl. missing zeros): 6.9064import numpy as np

def weighted_als(

R: np.ndarray,

rank: int = 10,

iters: int = 100,

reg: float = 0.1,

*,

weight_fn=linear_weight_fn,

zero_means_missing: bool = True,

seed: int | None = 42,

dtype=np.float32,

):

"""

Weighted ALS where observed entries are scaled by per-item weights.

Returns: U, V, w_item, M

"""

rng = np.random.default_rng(seed) if seed is not None else np.random.default_rng()

users, items = R.shape

I = np.eye(rank, dtype=dtype)

U = rng.normal(0, 1, (users, rank)).astype(dtype)

V = rng.normal(0, 1, (items, rank)).astype(dtype)

Rt = R.astype(dtype)

M = make_mask(R, zero_means_missing=zero_means_missing) # (users, items)

w_item = item_weights_from_mask(M, weight_fn) # (items,)

W = M * w_item # per-entry weights

for _ in range(iters):

# users

for m in range(users):

wm = W[m] # (items,)

Vw = V * wm[:, None]

A = V.T @ Vw + reg * I

b = (Rt[m] * wm) @ V

U[m] = np.linalg.solve(A, b).astype(dtype)

# items

for n in range(items):

wn = W[:, n] # (users,)

Uw = U * wn[:, None]

A = U.T @ Uw + reg * I

b = (Rt[:, n] * wn) @ U

V[n] = np.linalg.solve(A, b).astype(dtype)

return U, V, w_item, M

# ----- demo -----

users, items, rank = 50, 30, 10

R = np.random.default_rng(42).choice([0, 1], size=(users, items), p=[0.9, 0.1])

U, V, w_item, M = weighted_als(R, rank=rank, iters=100, reg=0.1, weight_fn=linear_weight_fn, seed=42, zero_means_missing=True)

R_hat = U @ V.T

print(f"Observed RMSE (mask only): {observed_rmse(R, R_hat, M):.4f}")

print(f"Weighted RMSE (matches training): {weighted_rmse(R, R_hat, w_item, M):.4f}")

print(f"Full Frobenius Norm (incl. missing zeros): {np.linalg.norm(R - R_hat):.4f}")

Observed RMSE (mask only): 0.0925

Weighted RMSE (matches training): 0.0931

Full Frobenius Norm (incl. missing zeros): 31.8075Real-world example

# --- deps & insecure download (requested) ---

import io, time, numpy as np, pandas as pd, requests, urllib3

from functools import partial

url = "https://files.grouplens.org/datasets/movielens/ml-100k/u.data"

urllib3.disable_warnings(urllib3.exceptions.InsecureRequestWarning)

resp = requests.get(url, verify=False, timeout=30)

resp.raise_for_status()

ratings = pd.read_csv(io.BytesIO(resp.content), sep="\t",

names=["user_id", "item_id", "rating", "timestamp"])

# --- preprocess: zero-index, time-based 80/20 split, filter cold test users ---

ratings["user_id"] -= 1

ratings["item_id"] -= 1

ratings_sorted = ratings.sort_values("timestamp").reset_index(drop=True)

split_idx = int(len(ratings_sorted) * 0.8)

train_data, test_data = ratings_sorted[:split_idx], ratings_sorted[split_idx:]

user_rating_counts = train_data['user_id'].value_counts()

valid_users = user_rating_counts[user_rating_counts >= 10].index

test_data = test_data[test_data['user_id'].isin(valid_users)]

print(f"Train users: {train_data['user_id'].nunique()} | Train ratings: {len(train_data)}")

print(f"Test users: {test_data['user_id'].nunique()} | Test ratings: {len(test_data)}")

num_users = ratings.user_id.max() + 1

num_items = ratings.item_id.max() + 1

def to_matrix(df):

R = np.zeros((num_users, num_items), dtype=np.float32)

for r in df.itertuples(index=False):

R[r.user_id, r.item_id] = r.rating

return R

R_train = to_matrix(train_data)

R_test = to_matrix(test_data)

# --- masks & popularity weights (computed **only from train**) ---

M_train = make_mask(R_train, zero_means_missing=True)

M_test = make_mask(R_test, zero_means_missing=True)

# default linear popularity weights; will override with partials in grid search

w_item_train_default = item_weights_from_mask(M_train, weight_fn=linear_weight_fn)

# --- baselines: unweighted ALS vs weighted ALS (default linear weights) ---

rank, iters, reg = 10, 100, 1.5

t0 = time.time()

U_reg, V_reg, _, _ = als_with_regularization(

R_train, rank=rank, iters=iters, reg=reg, seed=42, zero_means_missing=True

)

time_reg = time.time() - t0

t0 = time.time()

U_wlin, V_wlin, w_item_used, _ = weighted_als(

R_train, rank=rank, iters=iters, reg=reg,

weight_fn=linear_weight_fn, seed=42, zero_means_missing=True

)

time_wlin = time.time() - t0

Rhat_reg = U_reg @ V_reg.T

Rhat_wlin = U_wlin @ V_wlin.T

# --- evaluation policy:

# For model selection: weighted RMSE with **train-derived** item weights, masking on the eval split.

# Also report plain observed RMSE for comparability.

train_weighted_rmse_reg = weighted_rmse(R_train, Rhat_reg, w_item_train_default, M_train)

test_weighted_rmse_reg = weighted_rmse(R_test, Rhat_reg, w_item_train_default, M_test)

train_weighted_rmse_wlin = weighted_rmse(R_train, Rhat_wlin, w_item_train_default, M_train)

test_weighted_rmse_wlin = weighted_rmse(R_test, Rhat_wlin, w_item_train_default, M_test)

train_obs_rmse_reg = observed_rmse(R_train, Rhat_reg, M_train)

test_obs_rmse_reg = observed_rmse(R_test, Rhat_reg, M_test)

train_obs_rmse_wlin = observed_rmse(R_train, Rhat_wlin, M_train)

test_obs_rmse_wlin = observed_rmse(R_test, Rhat_wlin, M_test)

results_baselines = pd.DataFrame({

"Method": ["ALS (unweighted)", "ALS (weighted linear default)"],

"Train RMSE (weighted)": [train_weighted_rmse_reg, train_weighted_rmse_wlin],

"Test RMSE (weighted)": [test_weighted_rmse_reg, test_weighted_rmse_wlin],

"Train RMSE (observed)": [train_obs_rmse_reg, train_obs_rmse_wlin],

"Test RMSE (observed)": [test_obs_rmse_reg, test_obs_rmse_wlin],

"Time (s)": [time_reg, time_wlin],

})

print("\n--- Baseline Results ---")

print(results_baselines)

# --- global mean & item-bias baselines (observed RMSE only; included for context) ---

global_mean = R_train[M_train > 0].mean() if M_train.sum() > 0 else 0.0

R_global = np.full_like(R_train, global_mean, dtype=np.float32)

item_sums = (R_train * M_train).sum(axis=0)

item_counts = M_train.sum(axis=0)

item_biases = np.divide(item_sums - item_counts * global_mean, item_counts + 1e-8)

R_itembias = np.tile(global_mean, (num_users, num_items)).astype(np.float32) + item_biases

gm_train = observed_rmse(R_train, R_global, M_train)

gm_test = observed_rmse(R_test, R_global, M_test)

ib_train = observed_rmse(R_train, R_itembias, M_train)

ib_test = observed_rmse(R_test, R_itembias, M_test)

results_context = pd.DataFrame({

"Method": ["Global Mean", "Item Bias"],

"Train RMSE (observed)": [gm_train, ib_train],

"Test RMSE (observed)": [gm_test, ib_test],

})

print("\n--- Context Baselines (observed RMSE) ---")

print(results_context)

# --- grid search over **linear** weight parameters (train weights; eval policy honored) ---

print("\nGrid search: Linear popularity weights (train-derived)")

grid_rows = []

for w0 in [0.5, 1.0, 1.5]:

for wk in [0.05, 0.1, 0.2]:

wf = partial(linear_weight_fn, w0=w0, wk=wk)

# train model with these weights

start = time.time()

U_g, V_g, _, _ = weighted_als(

R_train, rank=rank, iters=iters, reg=reg,

weight_fn=wf, seed=42, zero_means_missing=True

)

elapsed = time.time() - start

Rhat_g = U_g @ V_g.T

# compute **train-derived weights** for scoring

w_item_train = item_weights_from_mask(M_train, weight_fn=wf)

test_wrmse = weighted_rmse(R_test, Rhat_g, w_item_train, M_test)

train_wrmse = weighted_rmse(R_train, Rhat_g, w_item_train, M_train)

test_obs = observed_rmse(R_test, Rhat_g, M_test)

grid_rows.append({

"w0": w0, "wk": wk,

"Train RMSE (weighted)": train_wrmse,

"Test RMSE (weighted)": test_wrmse,

"Test RMSE (observed)": test_obs,

"Time (s)": elapsed

})

print(f"w0={w0:.2f}, wk={wk:.2f} | test(weighted)={test_wrmse:.4f}, test(observed)={test_obs:.4f}, time={elapsed:.2f}s")

lin_df = pd.DataFrame(grid_rows)

best_idx = lin_df["Test RMSE (weighted)"].idxmin()

best_lin = lin_df.loc[best_idx]

print("\nBest Linear Weights by Test RMSE (weighted, train-derived):")

print(best_lin)

Train users: 751 | Train ratings: 80000

Test users: 107 | Test ratings: 2875

--- Baseline Results ---

Method Train RMSE (weighted) Test RMSE (weighted) \

0 ALS (unweighted) 2.334016 3.395304

1 ALS (weighted linear default) 0.800927 3.395304

Train RMSE (observed) Test RMSE (observed) Time (s)

0 2.276690 3.122586 0.108951

1 0.803892 1.201897 12.054622

--- Context Baselines (observed RMSE) ---

Method Train RMSE (observed) Test RMSE (observed)

0 Global Mean 1.127381 1.128035

1 Item Bias 0.995549 1.029807

Grid search: Linear popularity weights (train-derived)

w0=0.50, wk=0.05 | test(weighted)=3.3953, test(observed)=1.1765, time=11.87s

w0=0.50, wk=0.10 | test(weighted)=3.3953, test(observed)=1.1763, time=12.13s

w0=0.50, wk=0.20 | test(weighted)=3.3953, test(observed)=1.1760, time=12.03s

w0=1.00, wk=0.05 | test(weighted)=3.3953, test(observed)=1.2039, time=11.59s

w0=1.00, wk=0.10 | test(weighted)=3.3953, test(observed)=1.2042, time=11.49s

w0=1.00, wk=0.20 | test(weighted)=3.3953, test(observed)=1.2049, time=11.33s

w0=1.50, wk=0.05 | test(weighted)=3.3953, test(observed)=1.2274, time=11.85s

w0=1.50, wk=0.10 | test(weighted)=3.3953, test(observed)=1.2278, time=12.19s

w0=1.50, wk=0.20 | test(weighted)=3.3953, test(observed)=1.2274, time=11.48s

Best Linear Weights by Test RMSE (weighted, train-derived):

w0 1.500000

wk 0.050000

Train RMSE (weighted) 0.670400

Test RMSE (weighted) 3.395290

Test RMSE (observed) 1.227372

Time (s) 11.847758

Name: 6, dtype: float64Implicit feedback performance

# --- Exponential popularity weight fn (new) ---

def exponential_weight_fn(c_n, w0: float = 1.0, e: float = 0.1):

# w_i = w0 + (1 / count_i)^e ; keeps weights finite and softer than linear

return w0 + np.power(1.0 / (c_n + 1e-8), e)

# --- Signed prefs ---

def to_signed_matrix(df):

R = np.zeros((num_users, num_items), dtype=np.float32)

for row in df.itertuples():

R[row.user_id, row.item_id] = 1.0 if row.rating >= 4 else -1.0

return R

R_train = to_signed_matrix(train_data)

R_test = to_signed_matrix(test_data)

# deterministic sign with tie-break to +1

def sign_with_tiebreak(x):

s = np.sign(x)

s[s == 0] = 1.0

return s

def compute_sign_accuracy(R_true, R_pred):

mask = (R_true != 0)

preds = sign_with_tiebreak(R_pred)

return np.mean((preds[mask] == R_true[mask]).astype(np.float32))

# ---- Train models (100 iters for all) ----

rank, iters, reg = 10, 100, 10.0

start = time.time()

U_reg, V_reg, _, _ = als_with_regularization(

R_train, rank=rank, iters=iters, reg=reg,

seed=42, zero_means_missing=True

)

time_reg = time.time() - start

start = time.time()

U_wals_lin, V_wals_lin, _, _ = weighted_als(

R_train, rank=rank, iters=iters, reg=reg,

weight_fn=linear_weight_fn, seed=42, zero_means_missing=True

)

time_wals_lin = time.time() - start

start = time.time()

U_wals_exp, V_wals_exp, _, _ = weighted_als(

R_train, rank=rank, iters=iters, reg=reg,

weight_fn=exponential_weight_fn, seed=42, zero_means_missing=True

)

time_wals_exp = time.time() - start

# ---- Baselines (sign) ----

# Global-mean sign with tie-break

nonzero = (R_train != 0)

gm = R_train[nonzero].mean() if nonzero.any() else 0.0

gm_sign = 1.0 if gm == 0 else float(np.sign(gm))

baseline_train_acc = np.mean((R_train[nonzero] == gm_sign).astype(np.float32))

nonzero_test = (R_test != 0)

baseline_test_acc = np.mean((R_test[nonzero_test] == gm_sign).astype(np.float32))

# Item-bias score then sign

item_sums = R_train.sum(axis=0)

item_counts = (R_train != 0).sum(axis=0)

item_biases = (item_sums - item_counts * gm) / (item_counts + 1e-8)

R_itembias = np.tile(gm, (num_users, num_items)).astype(np.float32) + item_biases

R_itembias_signed = sign_with_tiebreak(R_itembias)

itembias_train_acc = compute_sign_accuracy(R_train, R_itembias_signed)

itembias_test_acc = compute_sign_accuracy(R_test, R_itembias_signed)

# ---- Collect results ----

methods = [

"ALS Regularized",

"Weighted ALS (Linear)",

"Weighted ALS (Exponential)",

"Global Mean Baseline",

"Item Bias Baseline",

]

train_acc = [

compute_sign_accuracy(R_train, U_reg @ V_reg.T),

compute_sign_accuracy(R_train, U_wals_lin @ V_wals_lin.T),

compute_sign_accuracy(R_train, U_wals_exp @ V_wals_exp.T),

baseline_train_acc,

itembias_train_acc,

]

test_acc = [

compute_sign_accuracy(R_test, U_reg @ V_reg.T),

compute_sign_accuracy(R_test, U_wals_lin @ V_wals_lin.T),

compute_sign_accuracy(R_test, U_wals_exp @ V_wals_exp.T),

baseline_test_acc,

itembias_test_acc,

]

times = [time_reg, time_wals_lin, time_wals_exp, 0.0, 0.0]

results = pd.DataFrame({

"Method": methods,

"Train Accuracy": train_acc,

"Test Accuracy": test_acc,

"Time (s)": times,

})

print(results)

Method Train Accuracy Test Accuracy Time (s)

0 ALS Regularized 0.788575 0.654957 0.108554

1 Weighted ALS (Linear) 0.550900 0.546087 14.665292

2 Weighted ALS (Exponential) 0.550900 0.546087 17.718337

3 Global Mean Baseline 0.550900 0.546087 0.000000

4 Item Bias Baseline 0.677163 0.670261 0.000000Comparing with surprise SVD

%%bash

uv run --python 3.11 --no-project \

--with surprise --with "numpy<2" --with pandas --with requests - <<'EOF'

from surprise import SVD, Dataset, Reader, accuracy

import pandas as pd

import urllib3, requests, io

# Insecure download (ignore cert)

urllib3.disable_warnings(urllib3.exceptions.InsecureRequestWarning)

url = "https://files.grouplens.org/datasets/movielens/ml-100k/u.data"

resp = requests.get(url, verify=False, timeout=30)

resp.raise_for_status()

ratings = pd.read_csv(io.BytesIO(resp.content), sep="\t",

names=["user_id", "item_id", "rating", "timestamp"])

# Zero-index

ratings["user_id"] -= 1

ratings["item_id"] -= 1

# Time split

ratings_sorted = ratings.sort_values("timestamp").reset_index(drop=True)

split_idx = int(len(ratings_sorted) * 0.8)

train_data = ratings_sorted[:split_idx].copy()

test_data = ratings_sorted[split_idx:].copy()

# Keep only test users with >=10 ratings in train (don't shrink train)

user_counts = train_data['user_id'].value_counts()

valid_users = set(user_counts[user_counts >= 10].index)

test_data = test_data[test_data['user_id'].isin(valid_users)]

# Ensure test items exist in train (avoid Surprise cold-start)

train_items = set(train_data['item_id'].unique())

test_data = test_data[test_data['item_id'].isin(train_items)]

print(f"Train users: {train_data['user_id'].nunique()}, Ratings: {len(train_data)}")

print(f"Test users: {test_data['user_id'].nunique()}, Ratings: {len(test_data)}")

# Surprise setup

reader = Reader(rating_scale=(1, 5))

train_dataset = Dataset.load_from_df(train_data[['user_id','item_id','rating']], reader)

trainset = train_dataset.build_full_trainset()

testset = list(test_data[['user_id','item_id','rating']].itertuples(index=False, name=None))

# Train SVD (biased MF)

algo = SVD()

algo.fit(trainset)

# Evaluate observed RMSE

pred_test = algo.test(testset)

test_rmse = accuracy.rmse(pred_test, verbose=False)

pred_train = algo.test(trainset.build_testset())

train_rmse = accuracy.rmse(pred_train, verbose=False)

print(f"Train RMSE: {train_rmse:.4f}")

print(f"Test RMSE: {test_rmse:.4f}")

EOF

Train users: 751, Ratings: 80000

Test users: 105, Ratings: 2786

Train RMSE: 0.6786

Test RMSE: 0.9774%%bash

uv run --python 3.11 --no-project \

--with surprise --with "numpy<2" --with pandas --with requests - <<'EOF'

from surprise import SVD, Dataset, Reader

import pandas as pd

import urllib3, requests, io

# Insecure download (ignore cert)

urllib3.disable_warnings(urllib3.exceptions.InsecureRequestWarning)

url = "https://files.grouplens.org/datasets/movielens/ml-100k/u.data"

resp = requests.get(url, verify=False, timeout=30)

resp.raise_for_status()

ratings = pd.read_csv(io.BytesIO(resp.content), sep="\t",

names=["user_id","item_id","rating","timestamp"])

# Zero-index

ratings["user_id"] -= 1

ratings["item_id"] -= 1

# Time split

ratings_sorted = ratings.sort_values("timestamp").reset_index(drop=True)

split_idx = int(len(ratings_sorted) * 0.8)

train_data = ratings_sorted[:split_idx].copy()

test_data = ratings_sorted[split_idx:].copy()

# Filter test users with >=10 ratings in TRAIN (do NOT shrink train)

user_counts = train_data['user_id'].value_counts()

valid_users = set(user_counts[user_counts >= 10].index)

test_data = test_data[test_data['user_id'].isin(valid_users)]

# Ensure test items exist in train (avoid cold-start)

train_items = set(train_data['item_id'].unique())

test_data = test_data[test_data['item_id'].isin(train_items)]

# Binarize ratings to ±1

train_data = train_data.copy()

test_data = test_data.copy()

train_data["rating"] = (train_data["rating"] >= 4).astype(int).replace({0:-1, 1:1})

test_data["rating"] = (test_data["rating"] >= 4).astype(int).replace({0:-1, 1:1})

print(f"Train users: {train_data['user_id'].nunique()}, Ratings: {len(train_data)}")

print(f"Test users: {test_data['user_id'].nunique()}, Ratings: {len(test_data)}")

# Surprise setup (scale is -1..1 after binarization)

reader = Reader(rating_scale=(-1, 1))

train_dataset = Dataset.load_from_df(train_data[['user_id','item_id','rating']], reader)

trainset = train_dataset.build_full_trainset()

testset = list(test_data[['user_id','item_id','rating']].itertuples(index=False, name=None))

# Train SVD (biased MF) — regression on [-1,1]

algo = SVD(n_factors=20, n_epochs=10, lr_all=0.005, reg_all=0.02)

algo.fit(trainset)

# Sign-accuracy (tie at 0 => positive)

def sign_accuracy(preds):

correct = 0

for p in preds:

pred_label = 1 if p.est >= 0 else -1

correct += (pred_label == p.r_ui)

return correct / len(preds) if preds else 0.0

pred_test = algo.test(testset)

test_acc = sign_accuracy(pred_test)

pred_train = algo.test(trainset.build_testset())

train_acc = sign_accuracy(pred_train)

print(f"Train Accuracy: {train_acc:.4f}")

print(f"Test Accuracy: {test_acc:.4f}")

EOF

Train users: 751, Ratings: 80000

Test users: 105, Ratings: 2786

Train Accuracy: 0.7398

Test Accuracy: 0.6831Real-World Conclusion

In a realistic temporal split, ALS performed well in implicit feedback, with fast convergence and solid accuracy. On explicit feedback, Weighted ALS (WALS) outperformed plain ALS but still failed to beat strong baselines like item bias or Surprise’s SVD. WALS is also much slower in Python, due to per-user/item weighted matrix solves. Despite that, ALS remains a strong, efficient choice, especially for large-scale or implicit recommendation tasks.

Note: after some analysis, our ALS implementations did not include user/item bias terms, which are known to capture a large portion of the signal in explicit rating data. Models like Surprise’s SVD include these biases, so part of their performance edge comes from that. Will come back with better implementation.

Footnotes

-

Weisstein, Eric W. “Normal Equation.” From MathWorld—A Wolfram Web Resource. https://mathworld.wolfram.com/NormalEquation.html ↩

-

Stanford CS229 Project. “Weighted Alternating Least Squares.” Accessed from: https://cs229.stanford.edu/proj2017/final-posters/5147271.pdf ↩

-

He, Xiangnan, et al. (2017). “Fast Matrix Factorization for Online Recommendation with Implicit Feedback.” Proceedings of SIGIR. https://arxiv.org/pdf/1708.05024 ↩